Returning to high prosperity, China's lithium battery industry chain achieved a year-on-year growth rate of over 40% in shipments in 2025.

01

According to preliminary research data from the High-tech Industry Research Lithium Battery Institute (GGII), China's lithium battery shipments reached 1,875 GWh in 2025, a year-on-year increase of 53%.

Among them, power battery shipments were 1.1 TWh and energy storage battery shipments 630 GWh, up 41% and 85% year on year respectively.

The share of LFP power batteries continued to rise. In 2025, shipments reached 882 GWh, surging over 130% year on year, accounting for 80% of total power battery shipments. The proportion hit new highs quarter by quarter and exceeded 82% in Q4 2025.

The energy storage industry is booming on both supply and demand fronts. In Q4 2025, shipments of energy storage lithium batteries rose over 20% month-on-month and more than 60% year-on-year. Insufficient capacity and frequent stock shortages have led to a rapid increase in OEM/contract manufacturing within the industry.

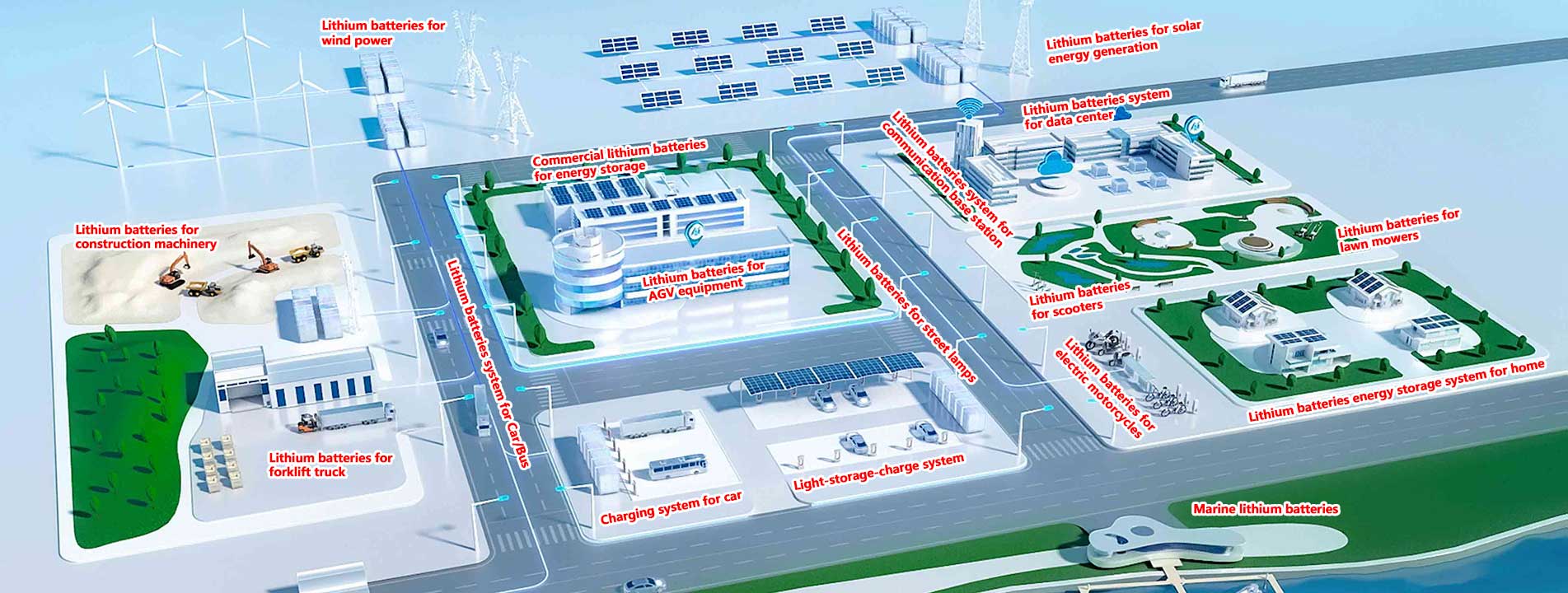

Segmented markets have entered an explosive growth phase. In 2025, lithium battery shipments in sectors such as construction machinery and electric vessels nearly doubled year on year.

02

Cathode material shipments rose 50% year on year, while shipments of the other three core lithium battery materials all posted a year-on-year growth rate of over 40%.

In the separator segment, limited new capacity will be added in the short term. Strong demand from the battery side is expected to usher in a new "spring" for shipments from second-tier manufacturers and enterprises that have newly entered the market in the past.

Similar to the energy storage industry, contract manufacturing became an important approach for new capacity expansion in the anode material industry in 2025, and the market temporarily entered a stage where "capacity is king".

China accounts for 94% of global electrolyte shipments. The scale advantage of China’s domestic electrolyte industry chain will remain strong in 2025–2026, and its share in the global market is expected to rise further.

In 2025, China’s electrolyte shipments reached 2.08 million tons, a year-on-year increase of 42%.

Prices of upstream raw materials for domestic electrolytes saw a rapid surge in Q3–Q4 2025. By the end of the year, domestic prices of VC (Vinylene Carbonate) and lithium hexafluorophosphate (LiPF₆) had exceeded 140,000 yuan/ton. The price of FEC (Fluoroethylene Carbonate) also broke through 70,000 yuan/ton, and prices are expected to continue rising in the future, with VC and LiPF₆ likely to surge past 200,000 yuan/ton again.

IPv6 network supported

IPv6 network supported